“You have power over your mind — not outside events. Realize this, and you will find strength.” Marcus Aurelius

In the wake of the COVID-19 pandemic, businesses lost revenues and workers lost jobs. But because of the time it takes to collect and collate data, economists have been left without much information to quantify the economic impacts at the local level.

But there is one ray of data illumination. Claims for unemployment benefits are promptly available and provide information about a large cross section of the economy. This post will outline what light unemployment claims data sheds on the state of the Uintah Basin’s economy.

While not all workers are protected by unemployment insurance laws, roughly 95% of jobs are covered. This makes claims data an exceptional source of information about the economy. Not included under unemployment insurance laws are most self-employed workers, about half of agricultural employment, unpaid family workers, railroad personnel (covered separately) and many nonprofit organizations (such as churches). Also, some out-of-work employees may not have worked a sufficient work history to qualify for unemployment insurance benefits, but may file anyway.

Fortunately, in this time of economic distress, the social safety nets of the unemployment insurance program, special national COVID-19 funding and social programs are working together to keep workers’ income and well-being stable.

Unemployment claimants and the unemployed; they aren’t the same

Also, keep in mind that, in addition to individuals drawing unemployment benefits, the unemployment rate includes those entering and re-entering the workforce and non-covered groups without current employment. This means the number of “unemployed” will be greater than the number of claimants. In “normal” times, only about 40% of the “unemployed” are claiming benefits.

The generally reported unemployment rate also has a work-search requirement. If you haven’t made any minimal attempts to find work, you aren’t counted as “unemployed.”

Watch this Space

While this analysis won’t be updated on a regular basis, new data will be added to the data visualization on a weekly basis allowing readers to check back for the latest information.

An Unprecedented Event

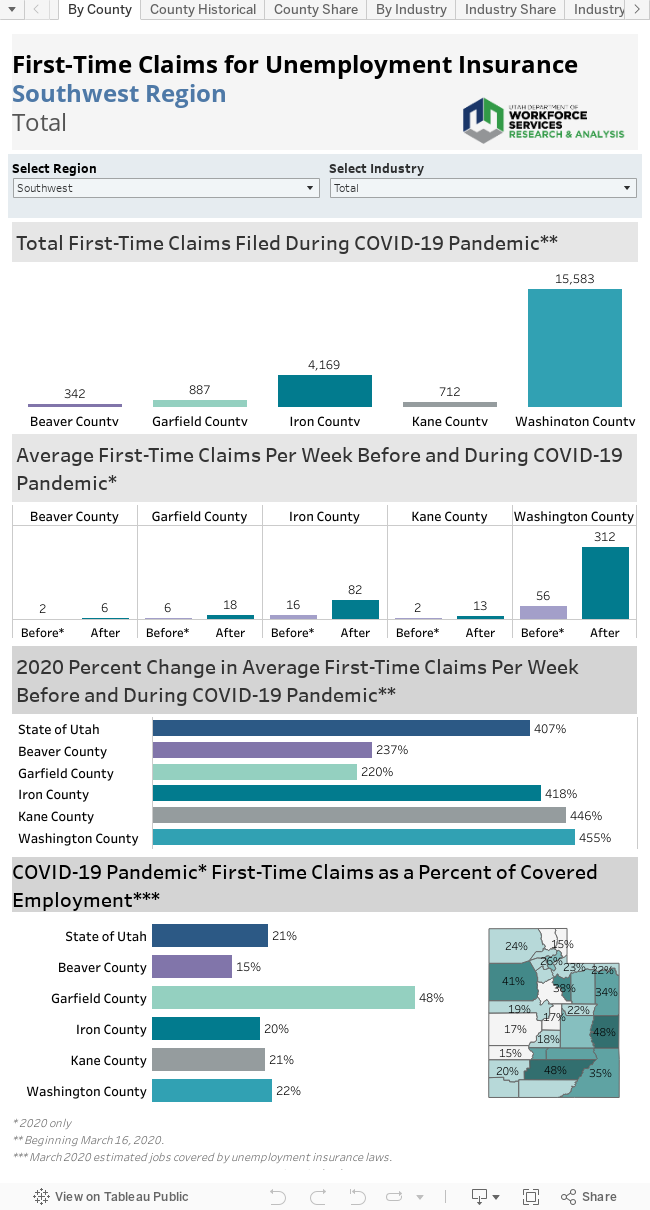

Not surprisingly, first-time claims for unemployment benefits soared in Utah and across the nation as the pandemic swept across the country. This increase is unprecedented since the creation of unemployment insurance coverage during the Great Depression. Week 12 (beginning March 16) marks the start of this unparalleled surge in claims. On a positive note, while new claims for unemployment benefits have skyrocketed in Utah, the state currently shows one of the lowest claims rates in the nation.

For the Uintah Basin counties, initial claims peaked in week 14. At the peak, initial claims totaled 500 between the three counties. By week 19, claims have decreased considerably. The levels are now comparable to levels seen during the Great Recession in the Uintah Basin.

Prior to the COVID-19 pandemic, counties in the Uintah Basin averaged 36 first-time claims per week. Afterwards, an average of 317 first-time claims were filed per week.

Who took the hardest hit?

Counties with large shares of accommodations/food service employment have been taking the hardest hit in the wake of the COVID-19 pandemic. This is true in the Uintah Basin as well, where 22% of the accommodations/food services workers in the area have filed claims for unemployment in the recent weeks.

Across all industries on a statewide level, 10% of the covered workforce have filled claims for unemployment benefits. Daggett County has been able to hold onto more of its workforce, with only 5% filing claims. Duchesne and Uintah Counties saw 11% and 13% of the workers file, respectively.

Tourism and COVID-19

Especially in the early stages of the restrictions, this is a story of tourism-dependent industries. Even with a relatively small portion of the Uintah Basin’s employment belonging to accommodations/food services, this industry made up for more than 14% of claims filed since the pandemic started. In addition, the true effect of the pandemic on this industry is masked by a large number of claims classified as industry “unknown” in the early days of the claims flood. Undoubtedly, many of these claims would rightfully be classified in accommodations/food services if the appropriate information were available.

Mining is a large share of the employment in the Uintah Basin and has also been responsible for a large amount of the claims filed — 21% of the regional claims. Retail trade, transportation/warehousing and healthcare/social assistance have also been high claims sectors.

The High and the Low

Although mining and accommodations/food services has generated the largest number of Uintah Basin initial claims in the COVID-19 time period, in percentage terms, other industries have actually suffered more. For example, the administrative support/waste management/remediation (which includes temporary employment services) sector has seen 45% of its workforce file for claims in recent weeks.

Although retail trade has seen a large number of claims, the percentage of its covered employment that has filed claims is relatively low at 7%. In other regions, retail trade saw a large share of the workforce file; but, in rural areas, a larger share of the retail establishments are likely deemed “essential,” meaning more of the workforce remained employed.

Public administration accounts for much of the Uintah Basin employment, and this is a sector that has kept a large share of its workforce employed, buoying the economy of the area.

County by County

Daggett County

• Prior to COVID-19, Daggett County had an average of one first-time unemployment claim per week. This has since increased to three claims.

• Public administration is an industry that has kept much of its workforce employed in the wake of COVID-19. With 49% of Daggett County’s workforce employed in the public administration sector, a relatively small percentage of the county’s covered workforce have filed claims for unemployment — only 5%.

• Like many other areas, the sector that suffered most from the restrictions was accommodations/food services. A significant 45% of this sector’s workforce filed claims for unemployment benefits.

• Prior to COVID-19, Daggett County accounted for 2% of the region’s unemployment claims, which has since decreased to 1%.

Duchesne County

• Prior to COVID-19, Duchesne County had an average of 11 first-time unemployment claims per week. This has since increased to 105 weekly claims.

• Mining and transportation/warehousing accounted for the largest numbers of claims in Duchesne County. Because these are such large industries in the area, the claims as a percentage of the workforce are relatively low — at 12% and 16% respectively.

• Public administration is also an important sector in Duchesne County and only 6% of that workforce has filed claims in recent weeks.

• Prior to COVID-19, Duchesne County accounted for 31% of the area’s unemployment claims. This has increased to 33% of the claims.

Uintah County

• Prior to COVID-19, Uintah County had an average of 24 first-time unemployment claims per week. This has since increased to 209 weekly claims — an increase of 774%.

• Mining and accommodations/food services have been the hardest hit sectors in Uintah County. Nearly 20% of the mining workforce in Uintah County has filed first-time claims for benefits in the wake of COVID-19. For accommodations/food services, more than 24% of the workforce has filed.

• Similar to the other counties in the region, public administration is an important sector in Uintah County. Only 1% of the workforce in that sector have filed claims, which helps offset some of the economic impact of some of the harder hit industrial sectors.

• Prior to COVID-19, Uintah County accounted for 67% of the area’s unemployment claims. This has decreased to 66% of the claims.

But there is one ray of data illumination. Claims for unemployment benefits are promptly available and provide information about a large cross section of the economy. This post will outline what light unemployment claims data sheds on the state of the Uintah Basin’s economy.

While not all workers are protected by unemployment insurance laws, roughly 95% of jobs are covered. This makes claims data an exceptional source of information about the economy. Not included under unemployment insurance laws are most self-employed workers, about half of agricultural employment, unpaid family workers, railroad personnel (covered separately) and many nonprofit organizations (such as churches). Also, some out-of-work employees may not have worked a sufficient work history to qualify for unemployment insurance benefits, but may file anyway.

Fortunately, in this time of economic distress, the social safety nets of the unemployment insurance program, special national COVID-19 funding and social programs are working together to keep workers’ income and well-being stable.

Unemployment claimants and the unemployed; they aren’t the same

Also, keep in mind that, in addition to individuals drawing unemployment benefits, the unemployment rate includes those entering and re-entering the workforce and non-covered groups without current employment. This means the number of “unemployed” will be greater than the number of claimants. In “normal” times, only about 40% of the “unemployed” are claiming benefits.

The generally reported unemployment rate also has a work-search requirement. If you haven’t made any minimal attempts to find work, you aren’t counted as “unemployed.”

Watch this Space

While this analysis won’t be updated on a regular basis, new data will be added to the data visualization on a weekly basis allowing readers to check back for the latest information.

An Unprecedented Event

Not surprisingly, first-time claims for unemployment benefits soared in Utah and across the nation as the pandemic swept across the country. This increase is unprecedented since the creation of unemployment insurance coverage during the Great Depression. Week 12 (beginning March 16) marks the start of this unparalleled surge in claims. On a positive note, while new claims for unemployment benefits have skyrocketed in Utah, the state currently shows one of the lowest claims rates in the nation.

For the Uintah Basin counties, initial claims peaked in week 14. At the peak, initial claims totaled 500 between the three counties. By week 19, claims have decreased considerably. The levels are now comparable to levels seen during the Great Recession in the Uintah Basin.

Prior to the COVID-19 pandemic, counties in the Uintah Basin averaged 36 first-time claims per week. Afterwards, an average of 317 first-time claims were filed per week.

Who took the hardest hit?

Counties with large shares of accommodations/food service employment have been taking the hardest hit in the wake of the COVID-19 pandemic. This is true in the Uintah Basin as well, where 22% of the accommodations/food services workers in the area have filed claims for unemployment in the recent weeks.

Across all industries on a statewide level, 10% of the covered workforce have filled claims for unemployment benefits. Daggett County has been able to hold onto more of its workforce, with only 5% filing claims. Duchesne and Uintah Counties saw 11% and 13% of the workers file, respectively.

Tourism and COVID-19

Especially in the early stages of the restrictions, this is a story of tourism-dependent industries. Even with a relatively small portion of the Uintah Basin’s employment belonging to accommodations/food services, this industry made up for more than 14% of claims filed since the pandemic started. In addition, the true effect of the pandemic on this industry is masked by a large number of claims classified as industry “unknown” in the early days of the claims flood. Undoubtedly, many of these claims would rightfully be classified in accommodations/food services if the appropriate information were available.

Mining is a large share of the employment in the Uintah Basin and has also been responsible for a large amount of the claims filed — 21% of the regional claims. Retail trade, transportation/warehousing and healthcare/social assistance have also been high claims sectors.

The High and the Low

Although mining and accommodations/food services has generated the largest number of Uintah Basin initial claims in the COVID-19 time period, in percentage terms, other industries have actually suffered more. For example, the administrative support/waste management/remediation (which includes temporary employment services) sector has seen 45% of its workforce file for claims in recent weeks.

Although retail trade has seen a large number of claims, the percentage of its covered employment that has filed claims is relatively low at 7%. In other regions, retail trade saw a large share of the workforce file; but, in rural areas, a larger share of the retail establishments are likely deemed “essential,” meaning more of the workforce remained employed.

Public administration accounts for much of the Uintah Basin employment, and this is a sector that has kept a large share of its workforce employed, buoying the economy of the area.

County by County

Daggett County

• Prior to COVID-19, Daggett County had an average of one first-time unemployment claim per week. This has since increased to three claims.

• Public administration is an industry that has kept much of its workforce employed in the wake of COVID-19. With 49% of Daggett County’s workforce employed in the public administration sector, a relatively small percentage of the county’s covered workforce have filed claims for unemployment — only 5%.

• Like many other areas, the sector that suffered most from the restrictions was accommodations/food services. A significant 45% of this sector’s workforce filed claims for unemployment benefits.

• Prior to COVID-19, Daggett County accounted for 2% of the region’s unemployment claims, which has since decreased to 1%.

Duchesne County

• Prior to COVID-19, Duchesne County had an average of 11 first-time unemployment claims per week. This has since increased to 105 weekly claims.

• Mining and transportation/warehousing accounted for the largest numbers of claims in Duchesne County. Because these are such large industries in the area, the claims as a percentage of the workforce are relatively low — at 12% and 16% respectively.

• Public administration is also an important sector in Duchesne County and only 6% of that workforce has filed claims in recent weeks.

• Prior to COVID-19, Duchesne County accounted for 31% of the area’s unemployment claims. This has increased to 33% of the claims.

Uintah County

• Prior to COVID-19, Uintah County had an average of 24 first-time unemployment claims per week. This has since increased to 209 weekly claims — an increase of 774%.

• Mining and accommodations/food services have been the hardest hit sectors in Uintah County. Nearly 20% of the mining workforce in Uintah County has filed first-time claims for benefits in the wake of COVID-19. For accommodations/food services, more than 24% of the workforce has filed.

• Similar to the other counties in the region, public administration is an important sector in Uintah County. Only 1% of the workforce in that sector have filed claims, which helps offset some of the economic impact of some of the harder hit industrial sectors.

• Prior to COVID-19, Uintah County accounted for 67% of the area’s unemployment claims. This has decreased to 66% of the claims.